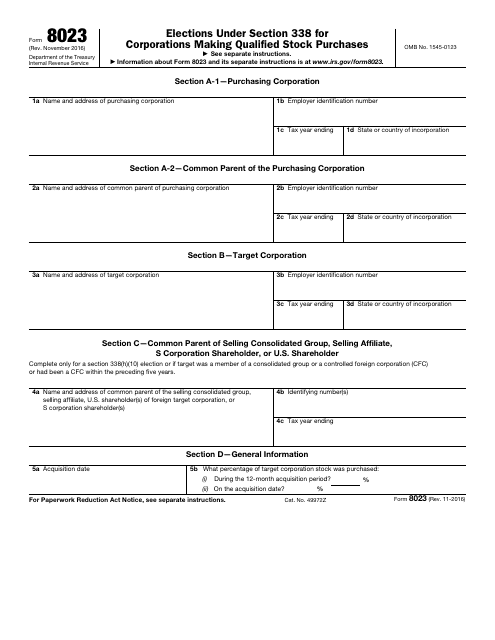

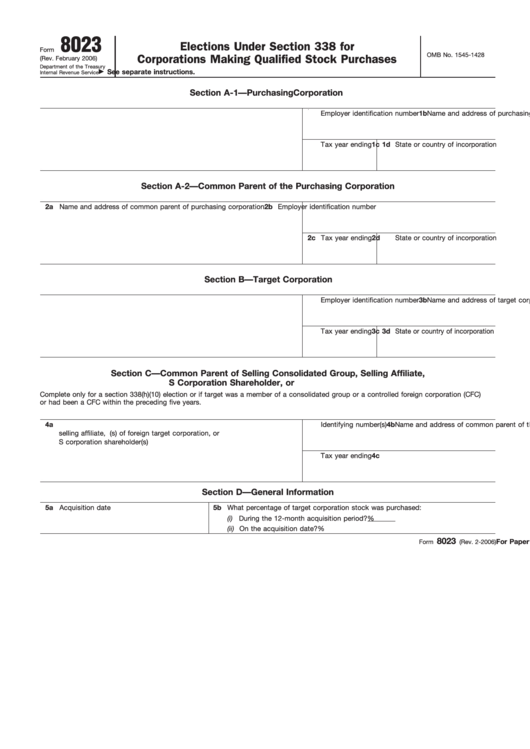

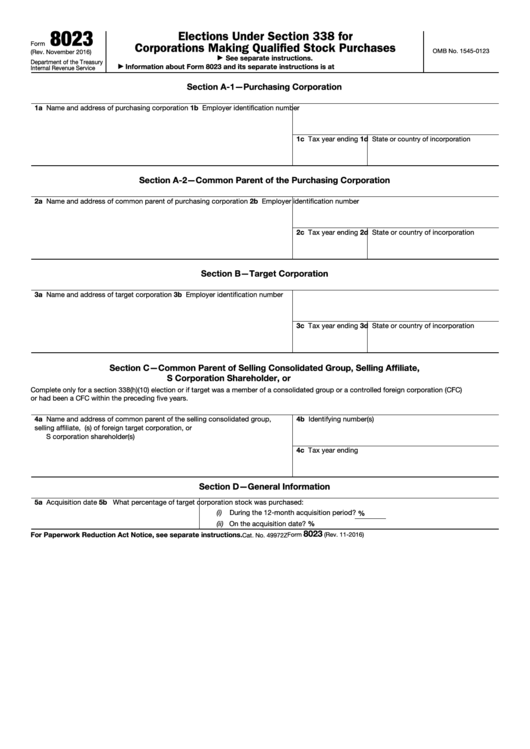

Form 8023 Instructions

Form 8023 Instructions - Unless otherwise specifically noted, the general rules and requirements in these instructions apply to foreign purchasing corporations. Web the form must be filed if the taxpayer meets both of the following conditions: Web we last updated the elections under section 338 for corporations making qualified stock purchases in february 2023, so this is the latest version of form 8023, fully updated for tax year 2022. Persons with respect to certain foreign corporations,” filed with respect to the purchasing corporation by each united states shareholder for the purchasing corporation's taxable year that includes. Web who must file. Information about form 8023 and its separate instructions is at. If a section 338 (h) (10) election is made for a target, form 8023 must be filed jointly by the purchasing corporation and the common parent of the selling consolidated group (or the selling affiliate or an s corporation shareholder (s)). Shareholders of controlled foreign purchasing. Web form 8023 must be filed as described in the form and its instructions and also must be attached to the form 5471, “information returns of u.s. , the irs is implementing the temporary procedure for fax transmission of form 8023, elections under section 338 for corporations making qualified stock purchases.

Generally, the purchasing corporation must file form 8023. November 2016) department of the treasury internal revenue service. , the irs is implementing the temporary procedure for fax transmission of form 8023, elections under section 338 for corporations making qualified stock purchases. (1) the taxpayer's worldwide gross income (defined in the form's instructions) in the tax year is more than $75,000, and (2) one of three specified criteria (described in the form's instructions) relating to residency in a u.s. Persons with respect to certain foreign corporations,” filed with respect to the purchasing corporation by each united states shareholder for the purchasing corporation's taxable year that includes. Web we last updated the elections under section 338 for corporations making qualified stock purchases in february 2023, so this is the latest version of form 8023, fully updated for tax year 2022. Information about form 8023 and its separate instructions is at. Web form 8023 must be filed as described in the form and its instructions and also must be attached to the form 5471, “information returns of u.s. Elections under section 338 for corporations making qualified stock purchases. Web about form 8023, elections under section 338 for corporations making qualified stock purchases.

(1) the taxpayer's worldwide gross income (defined in the form's instructions) in the tax year is more than $75,000, and (2) one of three specified criteria (described in the form's instructions) relating to residency in a u.s. , the irs is implementing the temporary procedure for fax transmission of form 8023, elections under section 338 for corporations making qualified stock purchases. Web about form 8023, elections under section 338 for corporations making qualified stock purchases. Selling shareholders if form 8023 is filed for a target Web the form must be filed if the taxpayer meets both of the following conditions: Web who must file. Shareholders of controlled foreign purchasing. Alternatively, form 8023 may be mailed to irs at the address provided in the instructions to. Web form 8023 must be filed as described in the form and its instructions and also must be attached to the form 5471, “information returns of u.s. Information about form 8023 and its separate instructions is at.

IRS Form 8023 Download Fillable PDF or Fill Online Elections Under

Web we last updated the elections under section 338 for corporations making qualified stock purchases in february 2023, so this is the latest version of form 8023, fully updated for tax year 2022. November 2016) department of the treasury internal revenue service. Generally, the purchasing corporation must file form 8023. Alternatively, form 8023 may be mailed to irs at the.

Form NAVSEA9243/5 Download Printable PDF or Fill Online Main Propulsion

Generally, a purchasing corporation must file form 8023 for the target. If a section 338 (h) (10) election is made for a target, form 8023 must be filed jointly by the purchasing corporation and the common parent of the selling consolidated group (or the selling affiliate or an s corporation shareholder (s)). Web form 8023 must be filed as described.

Fillable Form 8023 Elections Under Section 338 For Corporations

Selling shareholders if form 8023 is filed for a target Web who must file. Web form 8023 must be filed as described in the form and its instructions and also must be attached to the form 5471, “information returns of u.s. Web we last updated the elections under section 338 for corporations making qualified stock purchases in february 2023, so.

Health Screening Forms (COVID Form)

Generally, a purchasing corporation must file form 8023 for the target. Web we last updated the elections under section 338 for corporations making qualified stock purchases in february 2023, so this is the latest version of form 8023, fully updated for tax year 2022. November 2016) department of the treasury internal revenue service. , the irs is implementing the temporary.

Form 8023 Elections under Section 338 for Corporations Making

Special instructions for foreign purchasing corporations. Web we last updated the elections under section 338 for corporations making qualified stock purchases in february 2023, so this is the latest version of form 8023, fully updated for tax year 2022. November 2016) department of the treasury internal revenue service. Elections under section 338 for corporations making qualified stock purchases. Shareholders of.

Form 8023 Elections under Section 338 for Corporations Making

Web form 8023 must be filed as described in the form and its instructions and also must be attached to the form 5471, “information returns of u.s. Elections under section 338 for corporations making qualified stock purchases. Web about form 8023, elections under section 338 for corporations making qualified stock purchases. Shareholders of controlled foreign purchasing. (1) the taxpayer's worldwide.

Fillable Form 8023 Elections Under Section 338 For Corporations

Information about form 8023 and its separate instructions is at. Persons with respect to certain foreign corporations,” filed with respect to the purchasing corporation by each united states shareholder for the purchasing corporation's taxable year that includes. , the irs is implementing the temporary procedure for fax transmission of form 8023, elections under section 338 for corporations making qualified stock.

Cms 1500 Form Instructions 2016 Form Resume Examples MoYoGlEYZB

Web who must file. Shareholders of controlled foreign purchasing. Selling shareholders if form 8023 is filed for a target If a section 338 (h) (10) election is made for a target, form 8023 must be filed jointly by the purchasing corporation and the common parent of the selling consolidated group (or the selling affiliate or an s corporation shareholder (s))..

Cms 1500 Claim Form Instructions 2016 Form Resume Examples XE8je6e3Oo

Web about form 8023, elections under section 338 for corporations making qualified stock purchases. Shareholders of controlled foreign purchasing. Special instructions for foreign purchasing corporations. Generally, the purchasing corporation must file form 8023. Elections under section 338 for corporations making qualified stock purchases.

DA Form 8023r Download Fillable PDF or Fill Online Adult Mosquito

Web form 8023 must be filed as described in the form and its instructions and also must be attached to the form 5471, “information returns of u.s. Special instructions for foreign purchasing corporations. Web the form must be filed if the taxpayer meets both of the following conditions: Information about form 8023 and its separate instructions is at. If a.

Persons With Respect To Certain Foreign Corporations,” Filed With Respect To The Purchasing Corporation By Each United States Shareholder For The Purchasing Corporation's Taxable Year That Includes.

Web who must file. Selling shareholders if form 8023 is filed for a target If a section 338 (h) (10) election is made for a target, form 8023 must be filed jointly by the purchasing corporation and the common parent of the selling consolidated group (or the selling affiliate or an s corporation shareholder (s)). The irs will now accept taxpayers' completed form 8023 sent by fax to +1 844 253 9765.

, The Irs Is Implementing The Temporary Procedure For Fax Transmission Of Form 8023, Elections Under Section 338 For Corporations Making Qualified Stock Purchases.

Information about form 8023 and its separate instructions is at. Web about form 8023, elections under section 338 for corporations making qualified stock purchases. Elections under section 338 for corporations making qualified stock purchases. (1) the taxpayer's worldwide gross income (defined in the form's instructions) in the tax year is more than $75,000, and (2) one of three specified criteria (described in the form's instructions) relating to residency in a u.s.

Unless Otherwise Specifically Noted, The General Rules And Requirements In These Instructions Apply To Foreign Purchasing Corporations.

Generally, a purchasing corporation must file form 8023 for the target. Web we last updated the elections under section 338 for corporations making qualified stock purchases in february 2023, so this is the latest version of form 8023, fully updated for tax year 2022. Purchasing corporations use this form to make elections under section 338 for the target corporation if they made a qualified stock. Special instructions for foreign purchasing corporations.

Shareholders Of Controlled Foreign Purchasing.

Web form 8023 must be filed as described in the form and its instructions and also must be attached to the form 5471, “information returns of u.s. Generally, the purchasing corporation must file form 8023. Alternatively, form 8023 may be mailed to irs at the address provided in the instructions to. Web the form must be filed if the taxpayer meets both of the following conditions: